Outbound Mailer Script

STAGE 1: OPENING

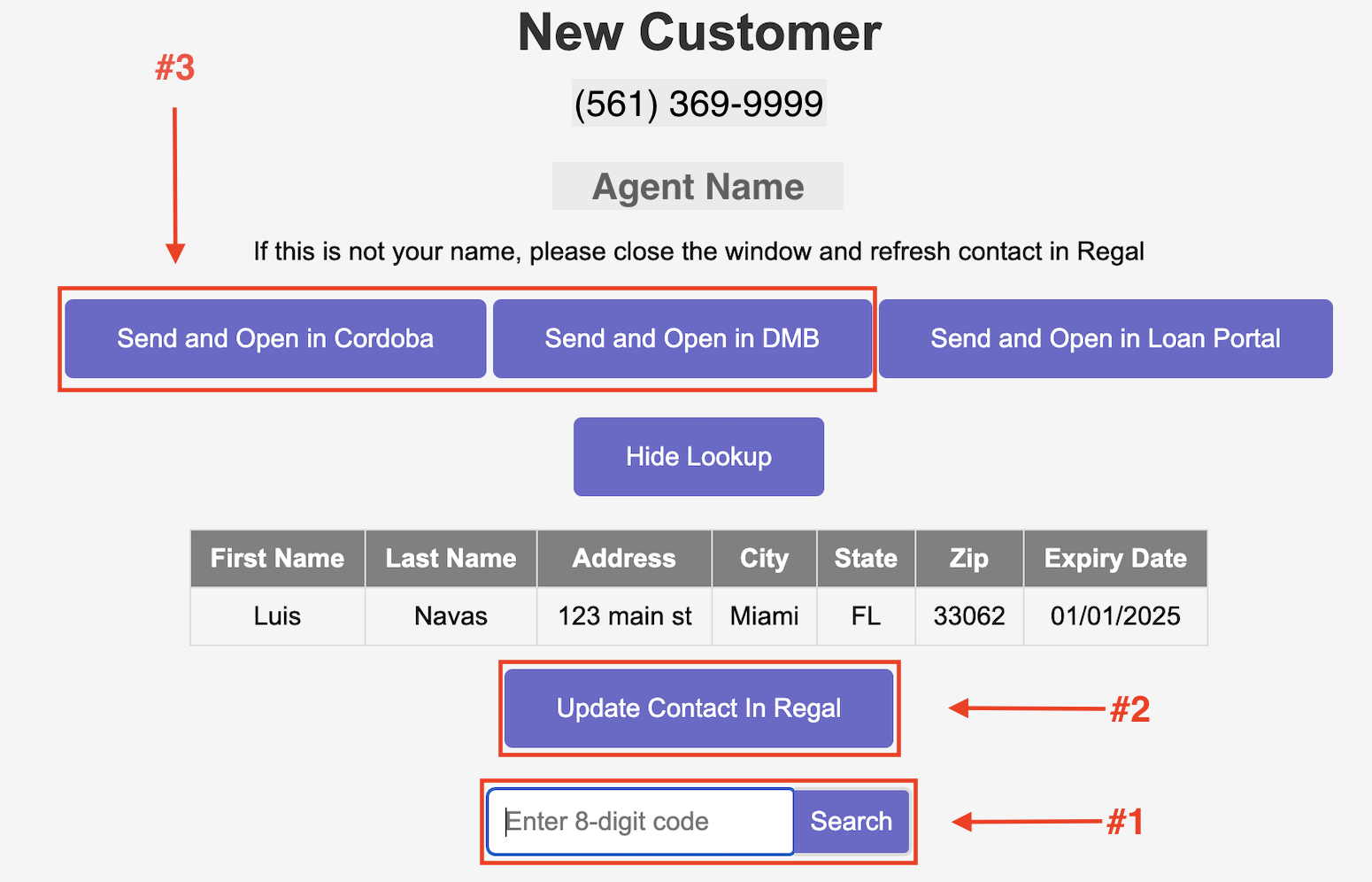

[REFRESH CONTACT IN REGAL AND OPEN BACKEND MANAGER]

Hi (client name), this is just (Rep Name) Senior Analyst with (Company Name). I just had a few moments before my next appointment to get back to you about the loan offer you received in the mail. How are you doing today?

Great, the fact that you received the mailer means that you may qualify for a debt consolidation loan.

HAS NAME: I see that you’ve already submitted your information online so please give me a moment to quickly pull up your file. (click open in backend – step #3)

NO NAME: Please provide me with the 8 digit invite code assigned to you from the mailer you received. This way I can look up some information about your offer. (their code is the last eight digits on the card they received in the mailer)

[The 3 steps below should only be used if you do not see customers name on lead or backend manager]

- Enter 8 digit offer code then click “search” to locate file

- Once you verify that you are speaking with the correct prospect, click “update contact”

- Select appropriate backend to send and the record will open in a new tab

I see here that I should be speaking with (Client Name) and you reside at (ADDRESS). Is that correct?

Now, before we go any further, let me provide you with my contact information so that in the event we get disconnected, you can get a hold of me directly. Sound good? You have something to write with to take down my info? Let me know when you are ready.

My name is (Rep Name). I am a Senior Analyst here at (Company Name).

My direct number to reach me is (rep direct line). You can email me at (rep email).

I show your number as (client number). Is that the best number to reach you? Is that your home, Cell phone or work number?

Now, (Client Name) most consumers call in for one of two reasons, let me know which reason best fits your situation.

They either want to pay off high interest credit card debt or

Consolidate credit card debt for a lower monthly payment.

Tell me, what best describes what you are looking to do?

Response: Listen, let them talk. Pause

If #1: Really? Tell me, how high are those interest rates? What is the monthly payment on those high interest rate cards? About how much?

If #2: Really? Tell me, how high are those monthly payments per month? Are those balances going down?

If neither #1 or #2, listen, agree, and somehow tie back to get a lower monthly payment on existing debt to help reach their goal.

OK, let’s start with some simple questions: (use concerned empathetic tonality)

Okay (client name) so can you walk me through what hardships you’ve experienced that helped create this situation? (BE EMPATHETIC and find common ground)

What’s making you want to take care of this now and what financial goals are you working towards?

[Listen, let the client speak and share their motivation to finally get rid of their debt: IDENTIFY AND FILL OUT HARDSHIP AND USE THROUGHOUT CONVERSATION AND TO DETERMINE WHICH QUESTIONS BELOW ARE APPROPRIATE]

So how long have you had this debt?

(If Applicable) – And you mentioned you’ve been paying ($$$) that entire time? “Yeah, I call it the pay forever plan, you pay endless interest to maintain and protect your credit and to try and avoid collections. But it’s literally like throwing money into the air because you never get anywhere with it. I understand how frustrating that can be.”

(If Applicable) Is that affordable to you or are you stretching things thin? – “It sounds like you could really use a lower payment. It would be great for you to just use your debit card for everything. That way you don’t keep compounding all of that interest. Let’s see how we can help.”

(If Applicable) Do you feel like you have been making progress paying down on these balances or do you feel like the majority of your payment is going towards interest?

Are you close to maxed out on some of these debts?

Was this debt acquired during COVID? “Okay that’s important to know for the application”

How’s your credit? – “Credit scores can always be repaired. I’m sure you already know they go up and down all the time, but you never get back all that money that you’ve been paying towards interest just trying to stay afloat and get by.”

How important is it for you to solve your debt problem and start saving money each month?

Thank you for that information. I’m confident that I will be able to assist you today.

STAGE 2: RUN AND REVIEW CREDIT

Okay, (Client Name) this process is straightforward. My job here is to help structure your application and present it in the best light to get you approved. The First Step is completing a short application and run a Soft Credit Check to review your credit report which will NOT impact your credit score. It’s a soft credit check. The credit check will help identify any debts you may be looking to pay off and consolidate. Second, we review your income and monthly expenses to determine a payment you can afford. From there, I will be able to either text or email you any possible approvals. Would that be appropriate?

Response:

Now, for the first step of pulling a Soft Credit Check, I am required to read you a disclosure. I must remind you that we are on a recorded line for compliance purposes. Understand?

Response:

READ DISCLOSURE:

IN ORDER FOR (Company Name) TO ORDER AND ACCESS YOUR CREDIT FILE, WE NEED YOUR AUTHORIZATION TO OBTAIN A COPY OF YOUR PERSONAL CREDIT REPORT FROM A THIRD-PARTY CREDIT REPORT PROVIDER. DOING SO IS PROVIDING “RECORDED INSTRUCTION” AUTHORIZING (Company Name) TO OBTAIN A COPY OF YOUR PERSONAL CREDIT REPORT IN ACCORDANCE WITH THE FAIR CREDIT REPORTING ACT. THIS PROCESS WILL HAVE NO IMPACT ON YOUR CREDIT SCORE. TO CONFIRM YOU AUTHORIZE US TO PULL YOUR REPORT, PLEASE SAY, “I AGREE.”

Response: I AGREE

Thank you for that, let’s continue…

What is your DOB?

And now go ahead and verify your SS# for me please… (be confident)

RUN CREDIT – Wonderful, this should not take long.

While waiting for the report to return, let me ask, have you applied for a loan with your local bank or any other lender recently? What were the results? (If not, why not?) Use some suggested conversation starters below:

Have you been shopping for a loan for a while? What were the results?

What prompted you to call today to find a solution with your debt?

Okay, I have your report now. Let’s review your debts to make sure the information is correct. Please grab a pen and paper so we can review this together.

[REVIEW DEBTS IN DEBTS TAB BUT ALSO PULL UP FULL CREDIT REPORT. ENCOURAGE PAY OFF OF ELIGIBLE DEBT AND DISCOURAGE INELIGIBLE DEBT.]

[Make it a conversation, let client speak, allow them to express their frustration and desire to pay-off or keep that debt. HARDSHIP]

I see (Name of Creditor) and you owe ($Balance). [Silence]

It shows an available limit of ($Limit). [Silence]

(If Applicable: Seems like you are maxed out and cannot use that card. [Silence]).

Are there any other unsecured debts that we may be missing? Like collection accounts, private student loans or unsecured loans that you would also like to consolidate?

Okay, in total, I see here you owe (Count off # of Accounts) with a combined balance of ($Balance) that you are currently paying monthly ($Monthly Payment). Does that sound correct?

Optional: (Perhaps share the link to the Bankrate.com credit card payment calculator) You know there is this useful tool offered by Bankrate.com. It’s a third-party website not affiliated with us. But it’s something I recommend to all my friends and clients. It’s simply a calculator that shows details about credit card debt and how to pay it off. You have access to the internet right now, let me text/email to you and let’s review it together.

[IDENTIFY 1 OR 2 OR THEIR MOST PROBLEMATIC ACCOUNTS]

USING A CONCERNED YET EMPATHETIC TONALITY SAY THE FOLLOWING:

Okay so (client name) have you considered the possible ramifications if you don’t do anything about your debt and your situation gets even worse?

Okay well after reviewing all this I definitely see where we can help and stop it from getting any worse than it already is. There’s just a few items on here that really jump out at me that I feel I really need to bring to your immediate attention…

[USING CREDIT REPORT WALK THE CLIENT THROUGH THE FORMULA BELOW TO PAINT THE PICTURE USING FACTS AND SIMPLE MATH]

IF CC: Limit Balance Min payment x # payments made.

$43,900 $50,020 $1284 x 48 = $61,632 (amount they’ve already paid)

“ Sir/Mam you may or may not be aware of this but you’ve already paid $61632 on a $43900 card but yet the balance owed is still $50020 after paying $1284 for the last 48 months. Based on these facts, does it seem to you like you’re getting anywhere with this? [silence let them reply] Exactly, and it’s not your fault – sadly for us consumers the terms are designed that way to keep us trapped in debt through all the compounding interest and fees but yet we continue to pay just to keep the card active thinking its helping your credit. On the brightside, it’s a good thing we’re on the phone so we can get you the help you need today.

IF LOAN: Limit Balance Term length x Min payment = Total paid at end of term

$2258 $2478 24 (months) x $391 = $9384

[sound concerned and empathetic] “Sir/Mam can I be straightforward with you? The terms on this loan are simply egregious. If you continued down this path you would end up paying $_____ on a $____ loan! Does that seem fair to you? I’m glad we’re speaking so that we can get you out from under these terms you’re in today.”

(If Applicable) So as you can see, your existing credit card terms can be improved. Mainly, your interest only minimum monthly payments are making it difficult to pay down on this debt. Have you noticed that?

You may or may not be aware of this but by continuing to make just the minimum interest only monthly payment on these debts, it would take you over a decade to pay this down. Realistically, you would need to pay at least three times the minimum payment to be on track to paying off this debt within a 60 month or five-year term. It’s not your fault. It’s a credit card trap.

Does that feel fair to you? (Listen, let the client speak and share their thoughts about their relationship with this debt. HARDSHIP)

Okay (Client Name), we are almost finished. It sounds like our goal is to get you a payment that fits within your budget so you can start saving money versus wasting your money. Are we on the same page?

At this point, give me a quick moment and together we can complete your application.

STAGE 3: COMPLETE LOAN APPLICATION – EMPLOYMENT, INCOME, AND MONTHLY BUDGET

Just as a reminder, my job here is to help structure your application and present it in the best light to get you an approval. I am confident that we can get you approved for something. With that being said, the next step is confirming your employment, income, and monthly expenses. We want to make sure to get you a payment you can afford.

COMPLETE REST OF CLIENT INTAKE FORM – MONTHLY BUDGET, INCOME, AND EXPENSES (REMEMBER UW GUIDELINES)

[BE CONVERSATIONAL. NOT CLINICAL. ]

Okay, so let me put you on a brief hold as I calculate some of the numbers for your monthly Debt-To-Income Ratio and make sure I structure this application in the best light to get you approved.

Okay, based on your income minus monthly expenses and credit card payments, I show here that you have $____ left over each month.

IF A LOT OF MONEY LEFT OVER: Does that sound correct? Where is all that extra money going? Do you have emergency savings or cash on hand in a bank account? If surplus go to continue.

(Try to call into question surplus liquidity in the face of high credit card debt. Try to get the consumer thinking about the need to consolidate.)

IF LOW: With only $___ left over each month, do you have any emergency savings? Do you have any other income sources or savings that can be verified with bank statements?

Okay, not to worry. All-the-more reason we need to consolidate your credit card debts and get you a lower monthly payment wouldn’t you agree?

OPEN CALCULATOR TO COMPARE WHAT THEY ARE PAYING NOW TO POSSIBLE PROGRAM PAYMENTS (do not quote payment yet!)

You currently pay $_____ per month on credit card bills. If we could consolidate and lower those payments by about half of what you’re paying now and get you debt free, would that be something that would work for you?

(The goal is to get the client into the mindset of consolidating debt and lowering their existing monthly payment.)

Okay (client name) just need a few more pieces of information to complete your application!

STAGE 4: SUBMIT TO LOAN PORTAL

[AFTER SAVING COMPLETED INTAKE FORM IN FORTH CRM, GO BACK TO BACKEND MANAGER -> CLICK “SEND TO LOAN PORTAL” TO OPEN LOAN PORTAL IN NEW TAB -> FIND YOUR LEAD UNDER “IMPORTED LEADS” SECTION -> CLICK “USE LEAD” -> COMPLETE LOAN APPLICATION]

“Okay, (Client Name), that’s everything I need to complete your application for submission… and we should have your loan results in just a moment. Now, I am going to walk you through the portal process. This is where we will be able to see what you are approved for. We can email the offers to you and review them together. Do you have access to your email?”

See guide for instructions if needed: LOAN PORTAL GUIDE

STAGE 5: REVIEW OFFERS AND PIVOT/PITCH

*If no loan offers SEE PIVOT

**If approved for Any Loan Offers read below THEN SEE PIVOT.

Okay, let’s look at your Offers… (review each offer with client)

What this means for this offer is that you are meeting the initial qualifications for an unsecured personal loan.

If you accept this offer, you will be working directly with (NAME OF LENDER). Their loan process is straightforward. They will require a hard inquiry credit check and proof of income and other identification documents to fund.

Based on your current profile these are the estimated terms being offered through this lender.

It appears the max amount you can finance is $_______. (Loan Amount)

(Identify if the loan amount is sufficient to cover the debts being considered for pay off. This may be an incomplete solution.)

Based on these terms, if you were to accept this offer, you would have a monthly payment of $____ on a term of _____ months based on an interest Annual Percentage Rate of ____%. There is no prepayment penalty with this offer.

Based on the payment and term you would be paying back a total of $______ of principal and interest.

What do you think?

If interested in this offer you can use the Link to complete the loan application process with that lender at any time. Before you consider this offer, let’s review some of the other offers you have been approved for.

(Repeat the process of reviewing each offer with the goal of demonstrating and having the consumer come to the conclusion that the Loan Offers presented are an incomplete solution that doesn’t benefit them.)

PIVOT [MAKE SURE TO SOUND EXCITED ABOUT THE APPROVAL FROM (Backend Company). EMPHASIZE HOW MUCH MORE THEY WOULD SAVE AND HOW MUCH MORE SENSE IT MAKES FOR THEM USING COST COMPARISON] [No Loan Approvals] (CLIENT NAME), so you don’t qualify for any traditional cash out loans, BUT congratulations because you do qualify for a hardship-based debt relief option with (Backend Company) that may offer a much higher savings. Given your current hardship this is a program that I was hoping you would qualify for and is much better suited for your unique situation. Let me explain it to you in detail, then you can ask any questions. [No Desirable Loan Approvals] (CLIENT NAME), though there isn’t a traditional loan approval that seems to be a good fit for you, congratulations because you do qualify for a debt relief option with (Backend Company) that offers a much higher savings. Given your current hardship this is a program that I was hoping you would qualify for and is much better suited for your unique situation. Let me explain it to you in detail, then you can ask any questions. (Continued) [PRICE OUT POSSIBLE PROGRAM IN ENROLLMENT TAB AND/OR USE CALCULATOR TO REINFORCE PROGRAM BENEFIT AND SAVINGS] (current payment) – (program payment) = (monthly savings) X (program term length) = (total savings) Please write this down. The new payment is $_____ over _____ months that takes care of the ______ accounts [Total Number of Qualified Debts] that can be included, which you’re currently paying $______ on… [List Included Debts] Now, compared to what you are paying now, this will save you $______ each month. “(client name) do you realize that now that you’ve been approved for this program by the end of it you will have $______ in your pocket at the end of this ____ months. When was the last time you had $_____ in the bank to use at your discretion?” I always love to ask my clients – what are you going to do with all that money you’re gonna save?! Do you think this could be the right answer since it would allow you to (recap client’s needs/goals as stated previously and/or the needs indicated by the Budget and Credit Profile)? |

|---|

(Let Client speak and share their thoughts. They need to fall in love with the monthly payment and savings before discussing details. Reinforce these positive feelings about this benefit.)

“As you can see, your existing terms with your creditors are preventing you from getting ahead. Your existing debt has impacted your credit and hindered your ability to pay down on this debt in any meaningful way. Currently, it will take you years to pay down on this and you will pay so much in interest while negatively impacting your credit. It is not your fault. It is these terms that these credit card companies have put you in. Do you agree?” (Discuss)

“Therefore, with this approval with (Backend Company), they will be reaching out to your creditors to get you better terms that will eliminate your high interest rates and finance charges while also reducing a portion of the principal balance owed. You will have a new payment with NO interest. That is how (Backend Company) is able to offer you this approval with a new low payment of $____ for only #_____ months. The best part is you’ll have a light at the end of the tunnel and a principal only payment that will pay down your balances. There is no prepayment penalty with this program so you can pay more if you like. Just keep in mind how much money this will be saving you each month.”

“Remember, it is important for (Backend Company) to get you these new terms so you don’t stay stuck in the situation that you are in now. Agreed?” (Discuss)

(They will most likely ask “how does this work”)

“Here’s how the process works.”

“First, this Approval is for a federally regulated hardship-based program. To clarify – this is NOT a government backed program, it just means it has federal laws in place that the program must adhere to for your overall protection and success. As such, your creditors will require that you demonstrate a hardship as you choose to stop making your monthly high interest payments to them.”

“To make this an easy and seamless process, there will be a FDIC insured trust account established in your name that you have full control over. Instead of making the minimum payments to your enrolled creditors, you will make one consolidated monthly deposit of ($ ) into your trust account.”

“As you make your new payments into your dedicated trust account, (Backend Company) will be reaching out to your creditors within the beginning stage of your program to work out new terms with them which usually cuts the balances down by about 50% or less on average.”

“Once these new terms are in place, you will be notified to authorize acceptance and payment of these new terms from your trust account to pay off your creditors.”

“They do this on every account until they are all at a zero balance.”

“This plan is not reported to the credit bureaus and there will be NO long-term negative effect on your credit like BK or credit counseling; just a temporary impact from nonpayment in the beginning of the plan, meaning as your debts are resolved and settled, your credit will begin to repair itself organically. As each account is paid off, one by one, your utilization will improve which will have a positive impact on your credit. Currently, your credit is slowly declining already. It’s not your fault. You just have to get rid of all this debt first. Do you agree? And once you pay off this debt through this program, you should see your credit improve.”

“Now, (client name) there are just two things you will have to do in-order for this program to work…”

“First, you must not use the enrolled cards any longer. You can open new credit lines in the future, but we suggest that you remain focused on staying debt free for now. If you do decide to take on new debt, remember to keep the balances low so you don’t end up with these terms we are getting you out of today. Make sense?”

“Second, we need to make sure the NEW payment is affordable so you do not miss any payments that you are making into your dedicated trust account. This will ensure your success in the plan.”

“Therefore, it looks like this payment of $______ is affordable to you based on your budget analysis. I know it’s less than what you’re currently paying now to your creditors but we still need to get final approval from UW on this.”

[REINFORCE VALUE OF PROGRAM – REFER TO COST COMPARISON CALCULATOR AGAIN IF NECESSARY]

STAGE 6: CLOSE

Once again, this is a hardship-based program. Due to COVID, many consumers are taking advantage of these programs. We have identified your hardship as follows:

INDICATE AND COMPLETE HARDSHIP [Silence: Allow Client to speak and discuss]

As such, it is important to remember that if you continue paying your creditors then they will not consider you to be in a true financial hardship. This can affect the ability of (Backend Company) to successfully negotiate on your behalf to get you the new terms. Remember, it is the current terms you are in right now that are keeping you from paying off this debt, right?

So, discontinue any auto drafts or payments to them from here on out and instead, we need to schedule your new lower monthly payment into the program with (Backend Company) so you can immediately start saving all that money each month.

Assuming the Close and Schedule 1st Deposit – Be CONFIDENT!

Okay, so ($$) per month for (# of months) and you’re out from under it. How often are you paid each month? (get pay frequency) As we discussed earlier the payments into the program are automatic and are typically scheduled around your pay schedule. When is your next payday? Okay so let’s go ahead and schedule your first payment for (2-3 days after pay date to allow payment to clear) to get you started. Would that be appropriate?

If NO – try to schedule within 5 days of next pay date. If still too soon, then ask when is best for them.

(Be Accommodating)

If YES – “Okay so your first payment will be on (date)”

Now, let’s schedule your recurring payment date. (Options and Accommodate) Remember, if you ever need to reschedule a payment date, that is not a problem. All you need to do is contact (Backend Company) and they can do that for you. You will be provided this information in your documents and in a Welcome Package after you enroll. Any questions?

As I mentioned, the payment is set up through auto draft. You will have access to manage your funds.

[OBTAIN AND INPUT BANKING INFO – BE CONFIDENT!]

Alright and do you want to use a checking or savings account for the payments? Is that account in your name? Ok and then go ahead with the routing number first whenever you’re ready – and the account?

STAGE 7: CONTRACT SIGNING

WALK CLIENT THROUGH AGREEMENT: CLG- WALK THROUGH 02-03-2022- final NEW.docx

Refer to contract signing walkthrough guide if needed: POWERPOINTDPP_FORTH.pptx

STAGE 8: SUBMIT TO UW

[REVIEW FILE TO MAKE SURE IT IS COMPLETE AND ACCURATE: IF EVERYTHING IS COMPLETE AND ACCURATE – THEN SUBMIT TO UW BEFORE REVIEWING QA QUESTIONS]

Okay, now that your file is complete, I am required to prepare you for your Quality Assurance Welcome Call. It is important that you understand the terms and conditions of the program for which you are enrolling. This is merely a formality, as you and I have discussed these matters already. But it is important you are familiar with the exact questions that will be asked and that you answer them correctly to ensure your file moves forward. If you have any questions, this is the time for you and I to address those while we are on the phone together as you may not have that opportunity on the QA call. If you do not answer the questions correctly on your QAW call, it may cause your file to fail and then we would need to start the process over. Okay?

[REVIEW PROPER QA WELCOME CALL QUESTIONS WITH CLIENT: Welcome Call Script.docx

STAGE 9: COMPLETE QA WELCOME CALL

[communicate with QA team on skype and confirm they are ready]

Everything checks out. We are almost complete.

At this stage, I will be transferring your call to Quality Assurance. They will go over the questions we just discussed and afterwards confirm some basic information. I may be on the line as well but not permitted to interrupt. Sound good?

Congratulations on taking your first steps to becoming Debt Free! If you ever have any problems or questions, help is just a phone call away. Please make sure to keep an eye out for any emails or texts from us or (backend company) over the next few days. Please write this down.

This is the customer service number for Cordoba Legal Group and they are available:

Monday – Thursday from 9am -9pm EST.

CLG Customer Service: 888-988-6815

Before I send you over for your welcome call, one thing we suggest clients do is to go online, log into your accounts and change the phone number you have on file with your creditors to our creditor hotline phone number. This way, they can handle that aspect for you and get all the calls and messages.

(Make sure you SUBMIT FILE Before Welcome Call)

Please write down this number: 561-560-3195. This is the number Cordoba Legal group uses for creditors.

Do you understand?

I would also like to schedule a brief call with you within the next 48 hours to simply review what we call the “keys to success” for your program. When is best for you?

Any final questions before I transfer you?

Wonderful, I am very excited and happy we could help you with your debt. You have all the contact numbers and you can even call me if you have any questions in the future. Thank you and congratulations on taking your first steps towards a debt free life!

Please hold while I transfer you in for your welcome call…

[TRANSFER CALL IN REGAL]

WELCOME CALL/QA: 561-560-3792

(ENTER CLIENT PHONE NUMBER TO FIND FILE)

WELCOME CALL TRANSFER

After dialing the Transfer # the system will ask you to select 1 for English or 2 for Spanish

It will then ask you to enter the phone number on that file ( Do Not Enter Anything but the Phone number on file).

After they pull up the file, they will ask you to transfer over for a quick welcome call.

Please do not stay on the line. The welcome call rep will let you know in Skype if the call was Completed or if they need to send it back to you so you can make any changes or if something needs to be buttoned up.

If ANY changes need to be made, you need to send the prospect a New Agreement to sign and then transfer back to the Welcome Call team.